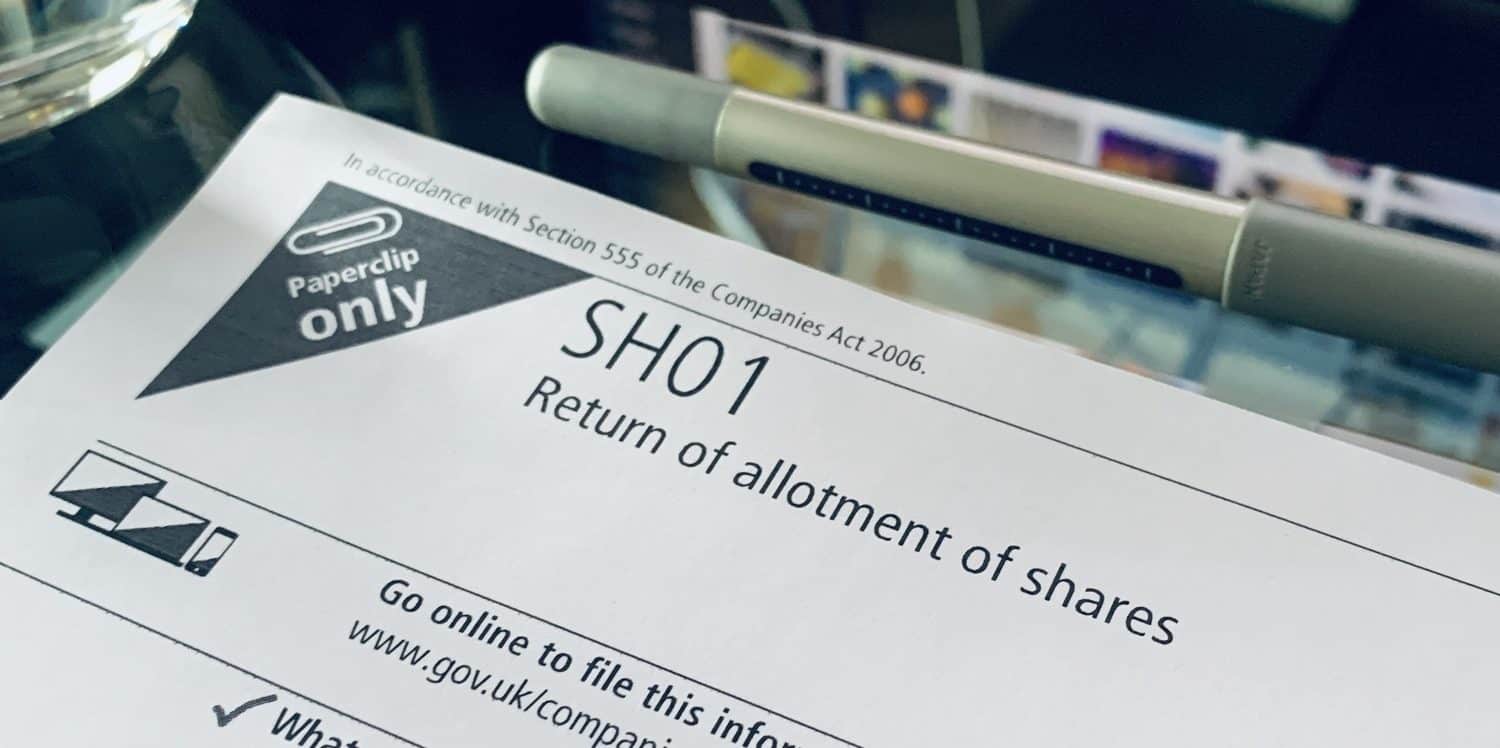

The Return of Allotment of Shares is the name of the Companies House form SH01. This form must be completed if you decide to issue (allot) new shares at any point after incorporation. You must deliver the Return of Allotment of Shares to Companies House within one month of an allotment.

Key takeaways

- To issue new company shares, you’ll need to complete the Return of Allotment of Shares (SH01) within one month after allotment.

- Verify pre-emption rights in your articles of association to protect existing shareholders during new share allotments.

- File a confirmation statement promptly after an allotment to ensure accurate shareholder records and compliance.

There are many reasons why people choose to issue more shares after company formation, such as:

- Raising additional capital from investors

- Repaying loans

- Funding a new project

- Awarding bonus shares to employees in place of cash bonuses

How to complete a Return of Allotment of Shares

The Return of Allotment of shares (Companies House form SH01) requests the following information:

- Registered name and number of the company

- Date of allotment

- Details of the new shares

- Details of shares issued for non-cash payments, if any

- Statement of capital

- Prescribed particulars of rights attached to the new shares

- Authorising signature

The Return of Allotment of Shares can be filed at Companies House online via WebFiling or by post. There is no need to provide the names of new shareholders on the form – this information should be included when you file your next confirmation statement (previously called an ‘annual return’). It is considered best practice to file a confirmation statement as soon as you can after an allotment.

Directors’ power to authorise share allotments

Generally, directors have the authority to allot new shares if the company has only one class of share, unless this power is expressly prohibited under the articles of association. To allot new shares in a company with more than one share class, directors must be authorised by a provision in the articles or by a special resolution of the members.

Check for pre-emption rights

Before allotting new shares, it is important to check the articles of association and shareholders’ agreement for pre-emption rights. If any such provision is in place, the existing shareholders have the right to purchase new shares before they can be offered to anyone else.

Join The Discussion