Turnover is a key metric for monitoring business performance, calculating taxes, and making informed decisions. Yet despite its importance, business turnover remains one of the most commonly misunderstood financial terms, often confused with profit.

Whether you’re launching a new startup or growing an existing business, understanding the meaning of turnover is vital for compliance, strategic insight, and operational efficiency. This guide aims to provide clarity and help you calculate your business turnover with confidence.

Key takeaways

- Turnover is your gross income from normal business operations during a specified period, excluding VAT, discounts, refunds, and non-operational revenue.

- It’s not the same as profit. While both metrics are key to understanding business performance, profit is what remains after deducting all costs and expenses from turnover.

- Accurate turnover tracking is essential for VAT registration, assessing eligibility for HMRC schemes, and obtaining finance and investment.

What is the meaning of business turnover?

Turnover refers to the total amount of income a business generates from its core activities over a given period, before deducting any costs or expenses (e.g., stock, wages, utilities, taxes). Essentially, it’s the gross revenue your business brings in. This includes income from:

- Selling goods or services

- Other expenses paid by the customer, such as commission, fees, processing charges, and shipping expenses

- Renting out property or leasing assets

- Royalties, licensing fees, and franchises

However, turnover does not include income from VAT charged on sales, investments, interest, asset disposal, or non-trading funds such as government grants, insurance payouts, and legal settlements. Additionally, customer discounts and refunds are not classed as turnover.

Businesses usually measure their turnover annually to track their performance and progress over time. But it’s equally important to measure it quarterly or monthly, especially when monitoring growth or staying within tax thresholds.

The difference between turnover and profit

Turnover and profit are equally important financial metrics for gauging business performance, but they are not the same. Understanding the distinction is crucial because they measure different things.

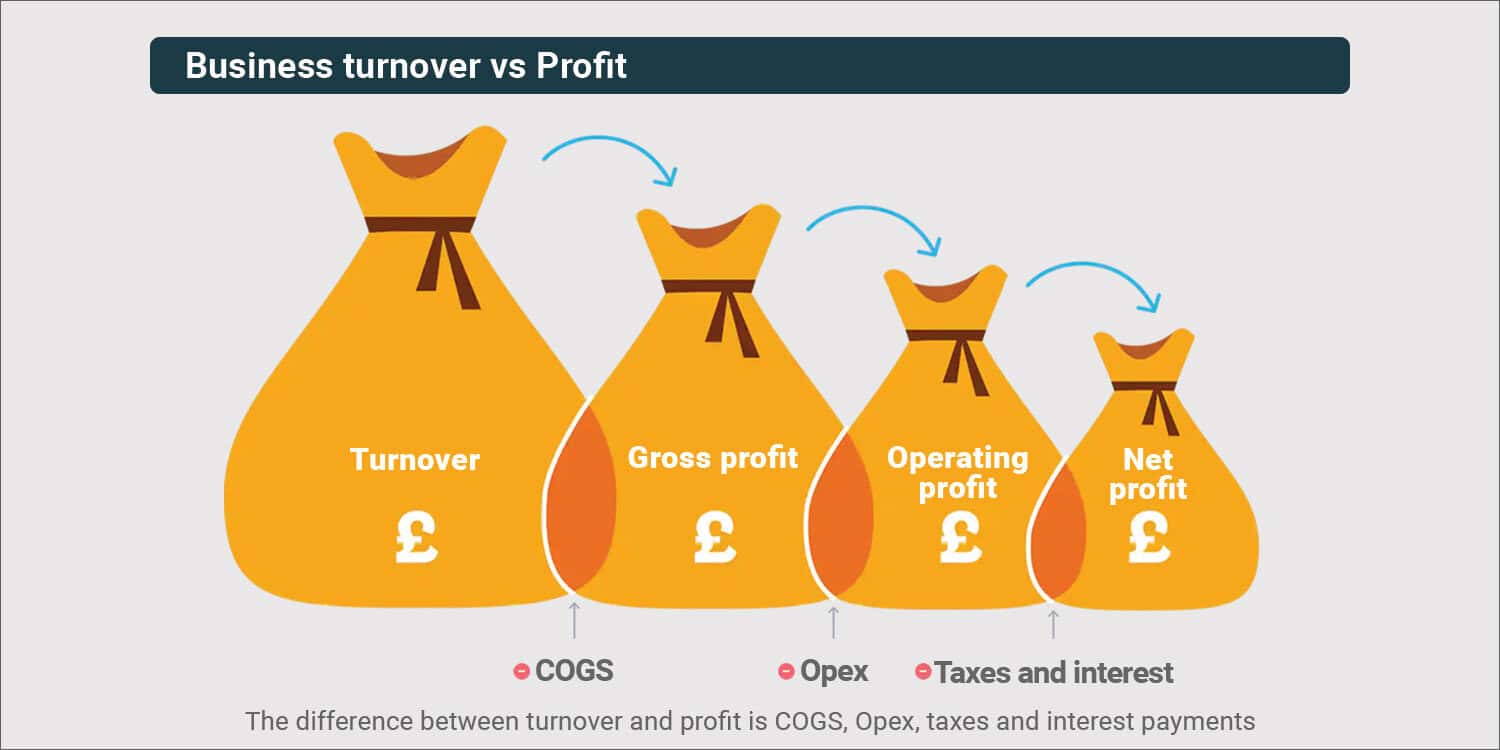

Turnover

Turnover is the total value of all goods or services that your business sells during a specified period before deducting any costs or expenses. It’s often referred to as the ‘top line’ because it’s usually placed on the top line of a business’s income statement (or profit and loss statement).

For example, if you sell 1,000 units at £100 each, your turnover is £100,000, regardless of how much it costs you to produce or supply those items.

Note that turnover is normally based on an accruals method. This means that sales that are still in debtors at year-end, rather than having been paid, are included, whereas cash received in a year for sales made in the previous year is excluded.

Profit

Profit is the amount of money your business is left with after you’ve deducted costs and expenses from turnover. It’s often called the ‘bottom line’ because it’s usually found at the bottom of a business’s income statement.

There are three main types of profit to consider: gross, operating, and net.

- Gross profit: Total business turnover minus cost of goods sold (COGS*)

- Operating profit: Gross profit minus operating expenses (Opex) such as rent, utilities, and wages

- Net profit: Operating profit minus all other business expenses, including taxes and interest

*COGS represents the direct costs associated with producing or delivering the goods or services your business sells, such as the cost of raw materials, wholesale stock, direct labour, and manufacturing overheads tied to the production process.

Gross profit and operating profit tell you how effectively your business is managing the direct costs of producing or supplying your products and maintaining day-to-day operations.

Net profit reflects how much money your business has made after meeting all costs, expenses, and taxes. It is the final indicator of a business’s profitability, and it’s the figure that most people mean when referring to ‘profit’. You can reinvest net profit back into your business, use it to pay debts, or distribute it to business owners.

Example

- Gross turnover = £100,000

- Less cost of goods sold = £25,000

- Gross Profit = £75,000

- Less operating expenses = £35,000

- Operating profit = £40,000

- Less all other costs and expenses = £15,000

- Net Profit = £25,000

Both turnover and profit are crucial to business success. The challenge is to achieve a high turnover while managing costs effectively.

Is business turnover the same as revenue?

Although the terms ‘turnover’ and ‘revenue’ are often used interchangeably, there is a subtle distinction between the two.

Both refer to the gross income a business receives from its core operating activities before deductions, but revenue also typically includes income from non-operating sources such as interest, investments, and asset sales.

However, many people also use the term ‘sales revenue’ when referring to business turnover.

Why is business turnover important?

While business turnover only tells part of the story, it is a key indicator of your business’s size and sales activity. As a flat figure, understanding and keeping track of turnover is important for several reasons:

1. VAT registration compliance

Turnover determines whether your business is legally required to register for VAT and start charging it on sales. The current VAT threshold is £90,000. If your taxable turnover exceeds this amount in any rolling 12-month period, you must register for VAT within a specified timeframe.

Use accounting software to set monthly automated reminders to check your rolling 12-month turnover. This will minimise the risk of late registration, which may attract a penalty.

Once VAT-registered, you can only cancel your registration if your taxable turnover falls below £88,000.

Taxable turnover for VAT is the total value of the goods or services (supplies) you sell that are not VAT-exempt or ‘out of scope’ for VAT. This includes standard-rated, reduced-rate, and zero-rated goods and services.

Be careful not to confuse ‘VAT-exempt’ and ‘zero-rated’ – they are not the same. VAT-exempt supplies are not subject to VAT, whereas zero-rated supplies are subject to VAT but at a 0% rate.

2. Eligibility for HMRC schemes

HMRC uses turnover to assess eligibility for certain tax reliefs or schemes such as the VAT Flat Rate Scheme, R&D tax relief, and Making Tax Digital for Income Tax.

3. Measuring performance

Turnover is an essential performance indicator, enabling you to evaluate market demand, operational efficiency, growth, and financial health over time.

It can show you whether your sales are increasing or decreasing and whether you need to make any adjustments to keep up with demand or address certain issues.

4. Determining company size

If you run a limited company, your turnover is one of three thresholds that determines your company size when preparing annual accounts for Companies House.

Micro-entities and small companies are usually exempt from audit and can submit simpler annual accounts than medium-sized and large companies.

5. Making informed decisions

Understanding your business turnover gives you a solid foundation for preparing accurate forecasts, setting goals, and making strategic decisions about the direction, management, and sustainability of the business.

If your turnover increases, this may indicate a need to employ more staff, increase inventory, move to larger premises, or invest in new technology. It could also be an opportunity to develop new products or services.

If turnover plateaus or slows down, you may need to consider your product quality, analyse market demand, improve your marketing efforts or sales strategies, reduce costs, or pivot your business.

6. Obtaining finance or attracting investment

Turnover is one of the first metrics that lenders and investors will look at. If you’re hoping to obtain a loan or bring in new shareholders, you’ll need to demonstrate that your business turnover is steady or increasing.

7. Applying for business insurance

When applying for business insurance, most providers will ask for your annual turnover to determine the appropriate level of cover for your business.

How to calculate your business turnover

Calculating business turnover is relatively straightforward, provided that you keep accurate financial and accounting records. Simply add all sales income (excluding VAT and any discounts) within a defined period.

Turnover formula: number of units sold x price per unit – VAT – discounts = total turnover

However, there are common pitfalls to be aware of to ensure your turnover calculations are accurate, consistent, and reliable:

1. Confusing turnover with profit

As previously mentioned, these two metrics are entirely different. Turnover is the total value of your sales revenue, while profit represents your business income after expenses.

2. Poor record-keeping

Failing to maintain meticulous records can cause errors in turnover calculations, accounts, and tax returns. Such oversights will make it challenging to monitor performance and prepare accurate financial statements.

3. Including VAT

If your business is VAT-registered, you must not include the VAT you charge on sales when calculating your turnover. VAT is not considered part of your business income – it is a consumption tax you collect on HMRC’s behalf.

- 25 financial terms every business owner should know

- Grow a small business: From solopreneur to building a team

- VAT terms you should know as a UK business owner

For example, if you sell an item for £100 and charge VAT at the standard rate (20%), the VAT cost will be £20, and your turnover will be £80.

4. Including discounts or refunds

Any special prices or discounts you provide to customers or select groups (e.g., employees, NHS workers, students) must be deducted from your turnover. You must only count the money that your business actually receives from sales.

Refunds to customers for goods returned or services cancelled must also be deducted when calculating your turnover.

5. Using inconsistent time periods

Using consistent time periods is crucial when calculating, analysing, or comparing turnover. Take care not to accidentally mix up reporting periods by combining sales figures from different months, quarters, or years.

6. Manually recording calculations

You’re more likely to make mistakes or miss small details when tracking business turnover manually. To avoid such issues, consider automating your processes using cloud-based accounting software like Xero, QuickBooks, or Sage.

These tools enable businesses to record and calculate turnover in real-time and perform comparative analyses of different time periods more easily.

7. Ignoring seasonality

To ensure accurate and meaningful insight into your business turnover, it’s essential to consider any seasonal fluctuations in demand, sales, and operational activity. Comparing turnover figures across different periods without considering seasonality will result in a distorted view of your business’s overall performance.

Thanks for reading

We hope you’ve found this post helpful and now understand the meaning and importance of business turnover. If you need better insights into your finances, consider working with a qualified accountant or integrating professional accounting software with your other business systems.

Looking to form a limited company to grow your business? Explore Rapid Formations’ range of company formation packages, with prices starting from only £2.99 (excluding the £100 Companies House fee).

Join The Discussion